What is a mortgage loan, and how does it work?

Understanding Mortgage Loans

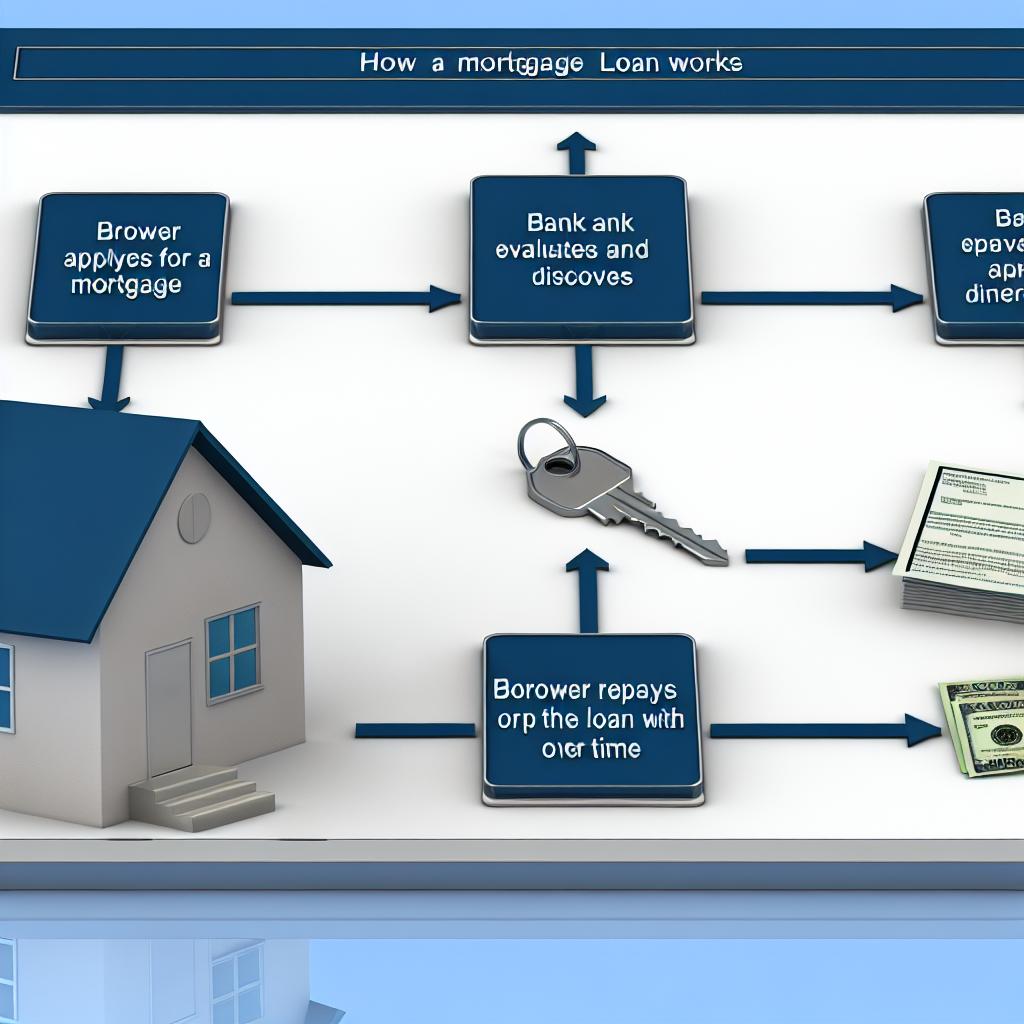

A mortgage loan is a financial arrangement designed specifically for the acquisition of real estate, whereby the property in question acts as collateral. Typically established between a borrower and a lender—which is often a bank or a financial institution—this arrangement permits individuals to purchase property without needing the full purchase amount at the time of transaction. It is essential for prospective homeowners or property buyers to comprehend the mechanics of mortgage loans, given the substantial financial commitment involved.

How Does a Mortgage Loan Work?

The process of acquiring a mortgage involves the borrower securing funds to buy a property. This money is then repaid over a predetermined period, which can usually span 15, 20, or 30 years, through consistent monthly payments. These payments generally consist of both the principal amount and interest.

The lending institution retains the property as collateral, which implies that if the borrower defaults on loan payments, the lender has the right to assume ownership of the property through an event known as foreclosure.

Key Components of a Mortgage Loan

Principal: This is the base amount of funds borrowed by the individual to purchase the property. With each payment made, the principal amount is gradually reduced.

Interest: Interest constitutes the expense incurred for borrowing the loan amount. The interest rate could be fixed—remaining constant throughout the loan term—or variable, subject to fluctuation based on market dynamics.

Property Taxes and Insurance: Typically, mortgage installments may cover property taxes and homeowner’s insurance. These are often managed by the lender through an escrow account to ensure timely payments.

Amortization: Mortgage loans are generally structured to be amortizing, ensuring that each monthly payment contributes to both the principal and interest. Initially, payments primarily address the interest component, but over time, they increasingly pay down the principal balance.

Types of Mortgage Loans

There are several variants of mortgage loans, each designed to fulfill specific financial conditions and objectives. Here are some commonly encountered types:

Fixed-Rate Mortgages: Loans offering a stable and unchanging interest rate over the lifecycle of the loan, providing predictability and security against market fluctuations.

Adjustable-Rate Mortgages (ARMs): These loans start with a lowered interest rate for an initial period, subsequently adjusting on a periodic basis, contingent on current market conditions.

Government-Backed Loans: These include options like FHA (Federal Housing Administration) loans and VA (Veterans Affairs) loans, each with specific eligibility conditions and benefits.

Qualifying for a Mortgage Loan

Acquiring a mortgage necessitates meeting certain financial criteria that lenders use to assess repayment capability. Generally, a good credit score, a favorable debt-to-income ratio, and stable income streams are needed. Lenders scrutinize these elements to ascertain an applicant’s financial health and repayment ability. Additionally, borrowers are usually expected to make a down payment, constituting a portion of the real estate’s purchase price.

Despite varying lender-specific prerequisites, understanding the general framework of mortgage qualification is instrumental for navigating the home-buying process. A firm grasp of mortgage terms, their types, and procedures places one in a better position to make well-informed purchasing decisions. For individuals seeking more comprehensive and authoritative insights, consulting resources like the Federal Reserve’s guide on mortgage loans can provide extensive knowledge on the workings and consequences associated with mortgage loans.

The Mortgage Application Process

Embarking on the journey of obtaining a mortgage requires understanding the multi-faceted application process. Highlighting essential steps can facilitate smoother navigation through this often-complex procedure:

Pre-Approval

Before seeking a potential property, obtaining pre-approval from a lender is often advantageous. Pre-approval entails submitting financial information to a potential lender who then evaluates it to decide the loan amount they could extend. This step is critical as it provides a clearer picture of how much one can realistically borrow, allowing for focused home search endeavors.

Choosing a Mortgage

Prospective buyers must select a mortgage product aligning with their financial standing and future goals. The choice between a fixed-rate mortgage, offering predictable payments, versus an adjustable-rate mortgage, which might initially offer lower rates, depends on individual circumstances and market forecasts.

Document Submission and Underwriting

Once a potential property has been identified and an offer accepted, the formal mortgage application demands comprehensive documentation. This typically includes employment records, bank statements, credit reports, and other financial disclosures, all required for the lender’s underwriting process. Underwriting involves a detailed assessment of an applicant’s financial history to confirm loan eligibility.

Closing Process

Upon successful underwriting, the closing process finalizes the mortgage agreement. This stage entails signing a myriad of documents detailing the loan terms and confirming the borrowed amount. During closing, associated fees and conditions set out in the loan agreement are also addressed. Post this procedure, ownership legally transitions, and the borrower commences payment installments as agreed upon in the mortgage terms.

Repaying a Mortgage Loan

Repayment of a mortgage loan is a pivotal aspect to comprehend. Typically extending over 15 to 30 years—except in cases of shorter loan terms—the repayment process involves amortized payments. Initially, the principal repayment is relatively low, while interest payments are higher. Over time, as the principal decreases, interest payments reduce correspondingly, enhancing the payment towards the principal.

Positive financial decisions during the loan term, such as additional principal payments or refinancing under favorable interest conditions, can notably reduce outstanding loan balances and interest amount payable over the loan duration.

In sum, understanding the underlying elements and processes involved in mortgage loans is vital for potential property buyers. Borrowers who are well-informed before stepping into the mortgage market can improve financial efficiency, ensuring they make prudent, long-term real estate decisions.